Packaging companies have a tough sustainability challenge—this industry sector has relied on materials like plastic since its onset, but in an age where landfills are overflowing and oceans are littered with plastic waste, they are under growing scrutiny from regulators and consumers to develop more circular, sustainable products, while others say packaging is no longer even necessary at all. And also of concern is that when packagers do offer sustainable services, consumers are often not even aware.

So there’s clearly a communication problem here, but that’s just the beginning. New research from global consultancy Bain & Company finds that nearly three-quarters (71 percent) of consumers in Europe say they want to buy sustainable products, and the same percentage of US consumers claim they want to buy products with as little packaging as possible. But while consumers are increasingly concerned, many struggle to identify sustainable packaging and aren’t even aware of what the most sustainable packaging materials are. For example, the firm’s survey of nearly 4,000 US consumers found that 70 percent believe single-use glass has a lower carbon footprint than single-use plastic, while only 12 percent guessed it was plastic—which is the correct answer.

According to the firm’s inaugural Global Paper & Packaging Report, retailers are responding. Most consumer product companies have publicly announced sustainability commitments. The problem is that brand owners still do not have a clear view on which packaging materials they prefer across different applications.

“Gone are the days when paper and packaging decisions were made based solely on cost, functionality, and consumer experience,” said Ilkka Leppävuori, global head of Bain & Company’s packaging group, in a news release. “Sustainability is now top of mind for everyone. However, when it comes to picking a packaging material—from paper to plastic to metal to glass—there’s no clear winner. Paper may have an edge, but the most sustainable option can vary greatly by application and geography. Leading companies are assessing the environmental impact of different materials and taking the full life cycle into account—from resource extraction and production to transportation and products’ end of life.”

And this is the crux of the comms issue in packaging—it seems every sustainable option also has its own drawbacks. The study reveals the hard choices the sector must make in choosing between materials, each with its benefits and tradeoffs from a sustainability standpoint. For example, the researchers’ analysis shows that while flexible plastics score best on production and transport related carbon emissions, they are the least circular or biodegradable.

Struggling to abate carbon emissions as the industry grows

The packaging sector could grow by 21 percent to reach $1.2 trillion in the next three years, with the largest growth coming from the rigid paper category, which may surpass plastic growth rates by 2026.

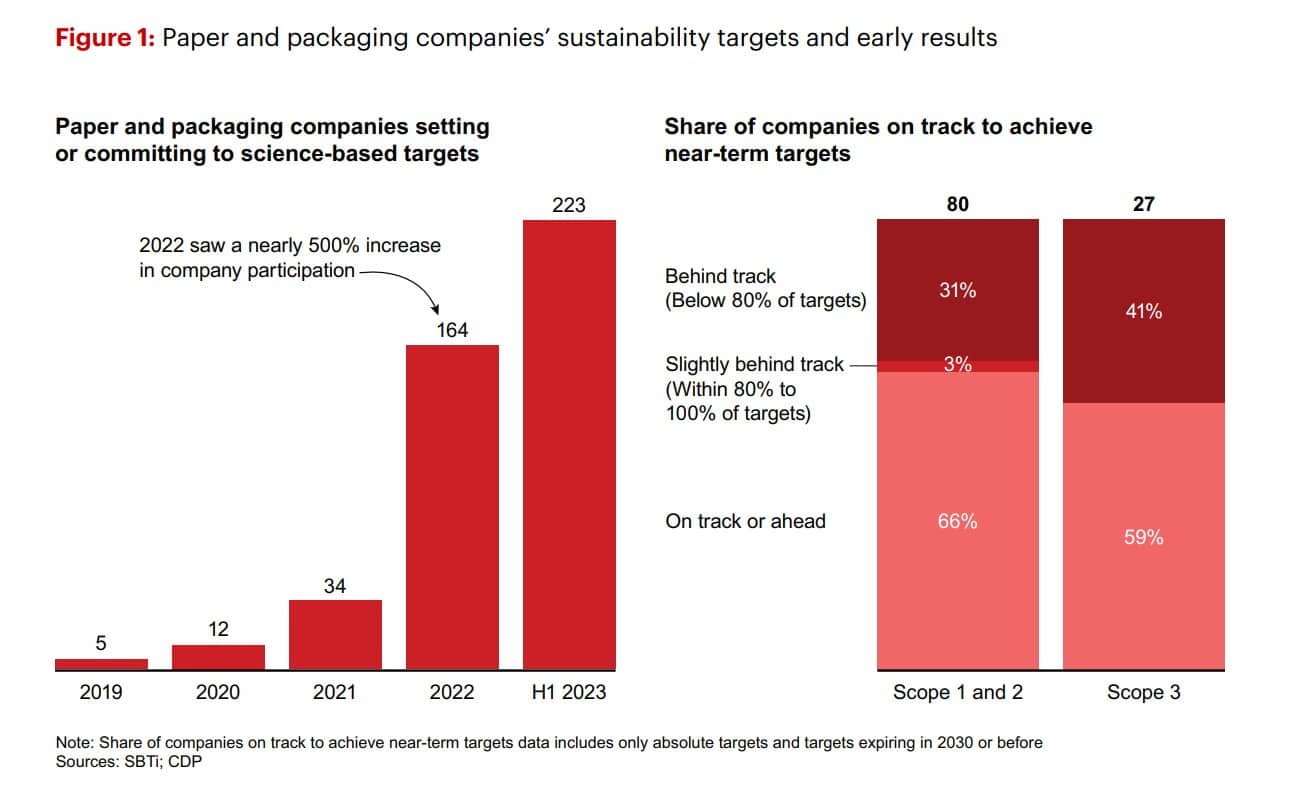

As the industry grows, so too do its decarbonization ambitions, but most paper and packaging companies can do much more. The number of companies in the industry that have verified or committed to science-based targets has increased from five in 2019 to 164 in 2022, yet more than 30 percent of those companies have missed their near-term Scope 1 and Scope 2 targets. Even more (41 percent) are missing their Scope 3 targets.

Creating value through sustainability

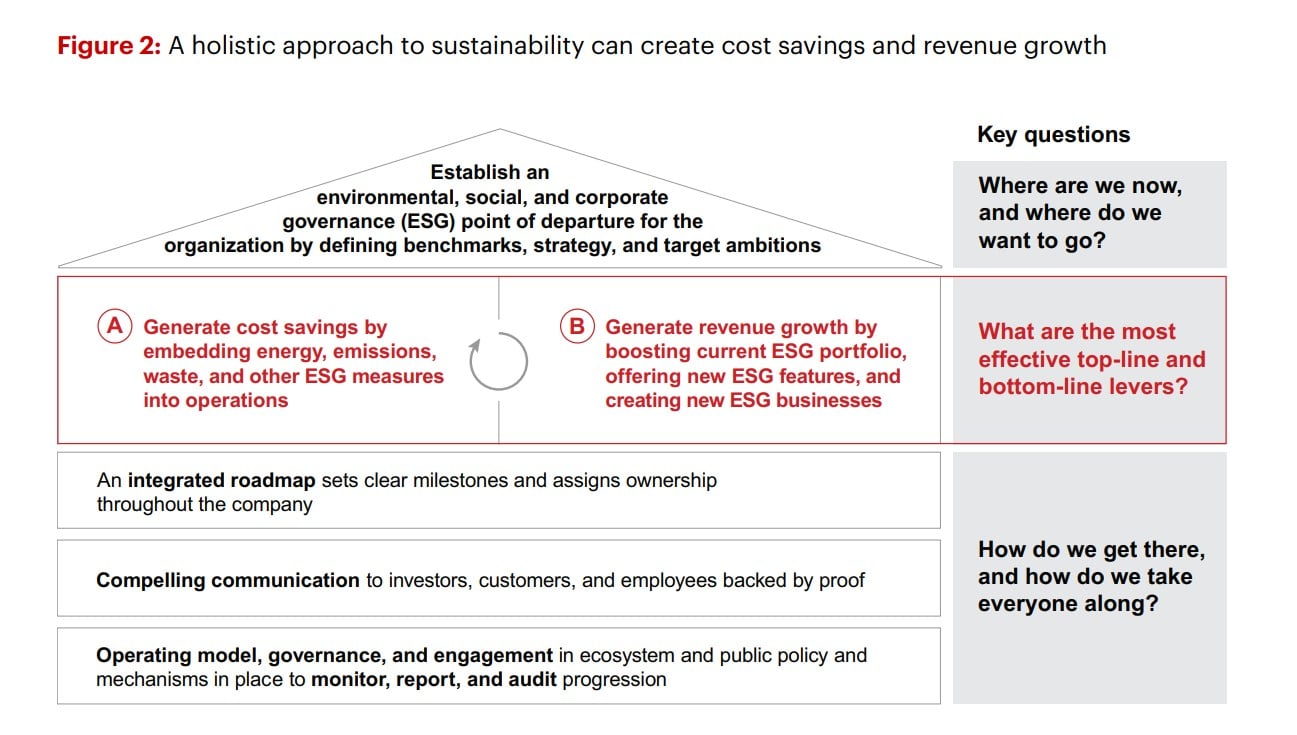

While, historically, executives have viewed sustainability initiatives as an extra expense to shoulder, leading companies realize a decarbonization and sustainability agenda can create economic value. Bain’s research shows two ways to create value through sustainability. They include cost savings and commercial or top-line growth. Leading paper and packaging companies are able to achieve a 4- to 6-percentage-point EBITDA increase through their effective use of cost savings and commercial levers.

Specifically, a sound sustainability strategy can reduce energy costs and increase access to recycled or renewable raw materials at a competitive cost. It can also help spur organic growth and price realization.

Biodiversity loss: the crisis facing the paper and packaging business

The paper and packaging industry has a significant impact on biodiversity, notably with regards to forestry management and water usage. Only 22 percent of companies surveyed reported assessing their value chain impact on biodiversity, and just 31 percent are acting now to address biodiversity loss.

Companies choosing to take action are poised to benefit by reducing their exposure to biodiversity-related risks as well as brand risks. Leaders are using sustainable forestry practices and increasing the share of recycled and reused materials to appeal to customers. Others are developing innovative packaging that enables them to target new markets with a lower carbon and biodiversity footprint.

The report explores a number of additional challenges and opportunities confronting the industry, including:

- Full potential transformation now includes net zero. The cross-functional effort to alter the financial, operational, and strategic trajectory of the sector now increasingly includes a concrete carbon reduction plan that outlines how to cut carbon emissions. When implemented successfully, the transformation can dramatically raise profitability, cash flow, top-line growth, and value.

- What does the mill of the future look like? The mill of the future is integrated and flexible, sustainable, and technology driven. Through optimization, it enables maximum productivity with high uptime and high asset health, lowering material consumption costs and minimizing waste. It is also adaptable, allowing various objectives, such as lower costs, reducing carbon emissions, or optimizing customer service. And it caters to a more fluid talent pool that changes jobs more frequently than in the past. Best-in-class mills that achieve true operational excellence can raise EBITDA by a seven percentage-point margin or more.

- Three ways to drive profitability. Paper and packaging companies can increase their EBITDA by 25-to-40 percent by addressing three areas. Many paper and packaging companies currently lack a robust view of profitability. Few understand how much share of wallet or business they could capture with existing customers. Many do not have a comprehensive list of new customers to pursue. Improving understanding across these domains will unlock significant growth.

- Embracing uncertainty. Supply and demand fluctuations, cost volatility in energy and raw material prices, and geopolitical risks have become the norm. The impact and timing of the green transition, new technologies, including artificial intelligence, smart packaging, and e-commerce penetration are also coming to the fore. Embracing uncertainty, scenario planning and future proofing is key.